BC Hydro will defer over a billion dollars of costs in the next three years without the independent approval of the BCUC. This could cause the Auditor General to qualify the provincial accounts (again).

The importance of fair public accounts

Most public companies record their costs in the year the costs are incurred. That way, everyone can see from the annual accounts how much profit they really earned. Lenders can decide how much to lend them, and at what price. Suppliers can decide whether they want to do business with them, and on what terms. A lot rides on our confidence in companies’ accounts being a true and fair picture of what actually happened.

Public accounts are important for governments, too. While governments do not earn profits, they do report either an annual surplus, if they take in more in taxes than they spend, or a deficit, if spending exceeds tax receipts.

A government’s public accounts are used to make sure tax dollars are being used wisely, and by investors who might consider buying the government’s bonds – needed if we are to keep funding those growing deficits here in BC (we already have enough problems with Moody’s downgrading our credit rating).

If the government were able to avoid recording some of its costs in the current year, it could make the deficit look smaller than it really is, misleading readers of the public accounts. In a 2019 report, the Auditor General of BC described this as the government “directing its own bottom line.”

To prevent this happening, accounting rules state that the government must record its costs in the year they are incurred. And the public accounts are audited by the Auditor General to ensure the rules have been followed.

Deferral accounts

But there’s an exception to the accounting rule about recording costs in the current year.

BC Hydro, the province’s largest electric utility, is a part of BC’s public accounts because it is provincially owned. Like all regulated utilities, it may sometimes “defer” some of its costs to future periods, if there’s a valid reason. For example, if there’s an unusual and short-term spike in costs, the regulatory principle of maintaining “rate stability” might justify spreading this cost increase out over a few years to avoid customers experiencing “rate shock.”

Deferred costs don’t show up in BC Hydro’s accounts for the year in which they are incurred, but are stored in a “deferral account” to be dealt with in future. And, since BC Hydro is part of the provincial government, the costs don’t show up in the budget deficit either (other things being equal, a deferred cost increases BC Hydro’s net income, which increases provincial revenue, which reduces the deficit).

Abuse of deferral accounts

You can see how it might be tempting for a government to take advantage of cost deferral. If BC Hydro were to defer some of its costs, voters might, temporarily at least, be deceived into thinking the provincial deficit was lower than it actually was. As a bonus, ratepayers might think that their lower rates were the result of good management on the part of BC Hydro or good stewardship by the government, rather than an accounting transaction.

To avoid these problems, the government and BC Hydro are not supposed to decide for themselves which costs to push out into the future. BC Hydro purports to prepare its financial statements in accordance with the International Financial Reporting Standards, which require that costs can only be deferred when this is approved by a “rate regulator” – the BC Utilities Commission (BCUC).

Role of the Auditor General of BC

The Auditor General is responsible for auditing the provincial accounts. This includes making sure that the accounts are consistent with accounting standards, and that they “present fairly, in all material respects, the financial position of government”, according to the audit report in the 2023/24 provincial accounts.

The provincial audit considers whether BC Hydro has only deferred costs that were approved by the BCUC – the rate regulator. If not, the Auditor General has a duty to say so publicly, by qualifying the accounts, a step it says “should be rare”. This unusual step is not just an embarrassment to the government, but may undermine public trust in government’s ability to administer public funds, and may even affect credit ratings and investor confidence, leading to a higher cost of public debt.

This happened in BC in 2016/17 and 2017/18. The Auditor General qualified the accounts because BC Hydro costs had been deferred by government order rather than by a decision of an independent regulator. This overstated both BC Hydro’s net income and the province’s surplus (those were the days…).

It almost happened again under the current government, when the Auditor General criticized BC Hydro’s third quarter 2022/23 results for failing to adhere to proper accounting standards, causing net income to be overstated by $265 million (and the provincial deficit to be understated by the same amount). The government had taken that money from a BC Hydro deferral account to pay for a bill credit to BC’s electricity customers. Thanks to the Auditor General’s criticism, BC Hydro reinstated the money in the deferral account, and the final year-end accounts were not qualified.

Current situation

So much for the history. What about today?

On March 17 the government ordered the BCUC to approve BC Hydro’s rates for the next two years. There’s plenty to dislike about this order, and at least one part of it may not even have been legal. But slipped in alongside the rate setting was a direction to the BCUC to approve $738 million of energy efficiency (or “demand-side management”) spending by BC Hydro for three years from 2024/25 to 2026/27.

This means there will be no review to ensure the $738 million spending is in the public interest (the test under section 44.2 of the Utilities Commission Act), but also that the BCUC has not independently approved BC Hydro’s deferral of the amounts to the Demand-Side Management regulatory account.

This is precisely the kind of behavior that the accounting standards set out to prevent, and which has caused the Auditor General to qualify previous provincial accounts.

Worse, the $738 million government direction overrides the BCUC’s previous approval of $110.1 million for 2024/25 with a new figure of $198.1 million. It appears BC Hydro was well over the original budget (third quarter results show that it had already racked up $115 million, with three months of the year left to run) and wanted retroactive approval for the spending.

There’s more

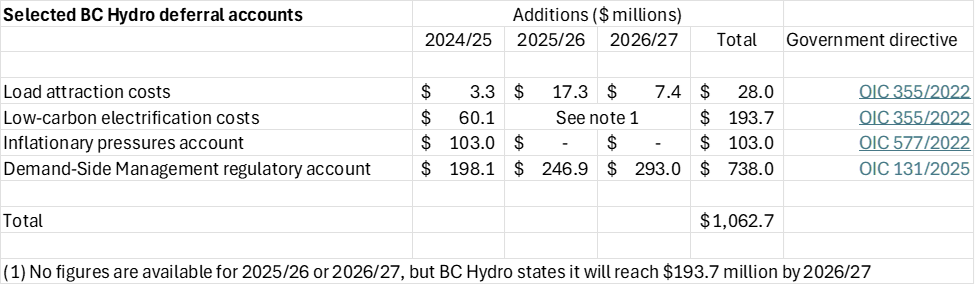

The $738 million deferral to the Demand-Side Management regulatory account is not the only cost deferral the BCUC has been directed to approve in the last few years. BC Hydro’s recent rates filing to the BCUC shows that at least a billion dollars of cost deferrals since 2024 that have been directed by government rather than the BCUC:

If one were concerned with costs being deferred without independent scrutiny, the amounts shown in the table above would be the place to start.

Net income

But if that weren’t enough, there’s also the matter of the government mandating BC Hydro’s net income.

In March 2024 the Auditor General said that the government’s directions to the BCUC to set BC Hydro’s net income were a “risk area” that might cause it to question the utility’s adherence to accounting standards. The Auditor General noted, perhaps more in hope than expectation, that the government’s latest net income direction was due to expire in March 2025.

Despite this stern warning from the Auditor General, in July 2024 the government extended yet again the direction that BC Hydro must be allowed to earn $712 million in net income. The BCUC is not permitted to determine whether the amount is fair, either to BC Hydro or to ratepayers.

Conclusion

The amount of government-directed cost deferral by BC Hydro has been creeping up in recent years, but the latest situation takes us back to the billion dollar-plus levels of the previous government.

With BC Hydro being such an integral part of the provincial accounts, it’s no longer clear that they “present fairly, in all material respects, the financial position of government.”

Perhaps the Moody’s credit rating agency is on to this. They forecast BC’s budget deficit this year will be $14.3 billion, far higher than the government’s own forecast of $10.9 billion. Are they taking these questionable cost deferrals into account?

It’s time for the Auditor General to take a look. Right now, though, BC only has an acting Auditor General. In an encouraging sign, she took on the Ministry of Forests recently, criticizing its calculation of the carbon benefit from forest investment projects.

Will she also be brave enough to challenge the government’s interference in BC Hydro’s use of deferral accounts?